PayPal and eBay Better Together

Strong synergies to lead future of commerce and digital payments

A global leader in a connected commerce world

eBay Inc. (Nasdaq: EBAY) today announced that it has issued the following letter to its shareholders. The company also said it has filed a definitive proxy statement with the Securities and Exchange Commission (“SEC”) with respect to eBay’s 2014 Annual Meeting of Stockholders, to be held on May 13, 2014.“Our shareholders and our customers are best served by keeping PayPal and eBay together,” eBay’s Board of Directors said. “No other payments competitor has achieved PayPal’s success—because no other competitor has had a commerce platform like eBay.”

The company reiterated five key reasons why PayPal and eBay are better together:

- PayPal Grows Faster Because of eBay

- eBay Accelerates the Success of PayPal

- Data Sharing Leads to More Profitable Growth

- eBay Inc. Provides Efficient Capital for PayPal

- Commerce and Payments are Converging

The full text of the letter is below.

March 24, 2014

Dear Fellow Shareholder:

Our company is a global commerce and payments leader operating in a rapidly changing landscape. Technology is creating a commerce revolution. The distinctions between online and offline commerce are disappearing. Mobile commerce is shifting consumer behavior. And retailers and brands of all sizes are adapting and innovating to engage consumers who have unprecedented choice in how they shop and pay. Scalable, flexible, integrated digital payments and commerce platforms are competitive advantages in this dynamic environment. That’s why we believe eBay Inc. is well positioned to lead and innovate globally, drive long-term growth and deliver sustainable shareholder value.

eBay’s Board of Directors and management team are singularly focused on doing just that – driving growth and increasing the value of your eBay investment over the long-term.

At our 2014 annual meeting, you have important choices to make. Activist investor and eBay shareholder Carl Icahn has submitted a non-binding proposal to spin off PayPal into a separately traded public company. He also has nominated two of his employees for election to eBay's board.

We have evaluated carefully Mr. Icahn’s proposal to spin off PayPal. We do not support it. Mr. Icahn’s proposal is not a new idea, and Mr. Icahn himself recently backed away from supporting his own proposal. The eBay Inc. Board of Directors has previously considered this idea closely. We also have had many discussions with shareholders. Our board is in unanimous agreement that neither Mr. Icahn's breakup proposal nor his nominees are in the best interests of eBay's shareholders. The eBay Board of Directors unanimously recommends that shareholders vote “AGAINST” Mr. Icahn's breakup proposal and “FOR” all four of the company’s experienced and highly qualified director nominees: Fred Anderson, Edward Barnholt, Scott Cook, and John Donahoe.

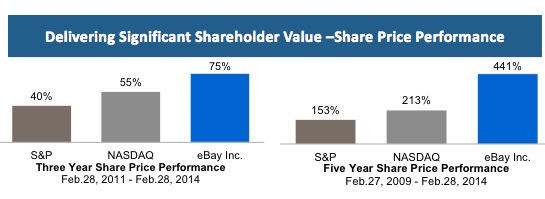

PayPal and eBay are better together. That’s been true for the past five years, during which time PayPal and eBay have generated a 441% increase in share price for our investors, significantly outpacing NASDAQ and the S&P. And we continue to believe today that PayPal and eBay together is the best path to creating sustainable shareholder value in the future. In today’s competitive environment, the advantages of PayPal and eBay together are more important than ever.

The eBay Story – Creating Value for Shareholders

Since our founding in 1995, eBay has been a leading global innovator in online commerce and digital payments, and the company has continually evolved to create and capitalize on technology-driven changes affecting the future of commerce and how consumers shop and pay. The board has engaged in constant dialogue with management about eBay’s strategic direction and has a clear track record of making the right decisions for eBay and its shareholders.

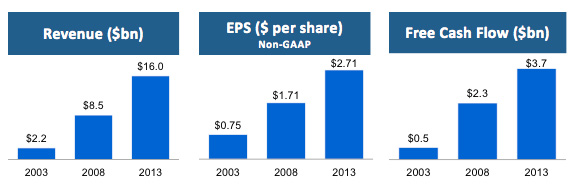

eBay has delivered phenomenal growth, resulting in substantial value creation for our shareholders.

Chart 1: eBay Inc. Annual Revenue – 2003, 2008 and 2013

Chart 2: eBay Inc. Annual Non-GAAP Earnings per Share – 2003, 2008 and 2013

Chart 3: eBay Inc. Annual Free Cash Flow – 2003, 2008 and 2013

Chart 4: eBay Inc. Shareholder Performance Over Three Years and Five Years

Payments is an integral part of commerce. Technology, led by mobile, is creating a convergence of payments and commerce capabilities across our industry. eBay Inc. is a leader in this evolving competitive environment. And since its acquisition in 2002, PayPal has thrived as part of eBay Inc., becoming a global leader in digital payments.

PayPal and eBay together have enabled us to drive mobile commerce and payments leadership, a competitive strength given the role mobile is playing in altering the commerce landscape. In 2009, we launched an aggressive push into the nascent mobile commerce space. eBay mobile was an early leader, and the eBay mobile app has been downloaded more than 186 million times since launch. In the three-year period 2010-2013, PayPal’s mobile payments volume increased 36 times. Today, our company is a clear leader, with eBay reaching $22 billion and PayPal hitting $27 billion in mobile commerce volume in 2013.

As we compete in the $10 trillion commerce market, we believe that the opportunity for dramatic growth for eBay and its shareholders is larger than ever before. Some of the most important trends in commerce – including online/offline convergence, mobile, social, data, the app economy, evolving payment systems – align with eBay assets and position us well for the future. Our 2013 performance, including 14% year-over-year revenue growth, 15% year-over-year non-GAAP earnings per share growth and $3.7 billion in free cash flow, demonstrate we are on the right path.

The eBay Board – The Right Team to Lead eBay into the Future

We’ve been able to build this thriving business thanks to our high quality management team and board. This is a group with deep experience in technology and financial services, a track record of tremendous value creation and significant ownership in the company. They have unrivaled experience and strong track records in and outside of eBay. And each has helped lead meaningful shareholder value creation during their tenure.

- John Donahoe became CEO of eBay in 2008 and immediately ushered in a series of changes that transformed both the company's leadership team and its strategic position. Prior to joining the company in 2005, John led global management consulting firm Bain & Company. Over the past five years, John has lifted eBay annual revenues 88%, total payment volume 199% and share price 441%.

- Fred D. Anderson is co-founder and managing director of the private equity firm Elevation Partners. He previously served as CFO of Apple, where he was considered to be one of the driving forces behind Apple's turnaround. During his tenure at Apple, its stock price increased by over 1,000%. He has helped eBay focus on efficient, low-cost funding of PayPal's growth domestically, including through the use of offshore cash.

- Marc L. Andreessen is co-founder of the venture firm Andreessen Horowitz. He's among the Internet's founding fathers, as a creator of the pioneering Mosaic Web browser and co-founder of Netscape. Marc is sought out by many for his entrepreneurial background, his views of the evolving technology landscape and his investment acumen - he also serves on the boards of Hewlett-Packard and Facebook - and has contributed to helping us innovate and develop our leading technology platforms, acquire companies, and grow our business.

- Edward W. Barnholt served as President and CEO of Agilent Technologies, a provider of test and measurement equipment, from May 1999 until his retirement in March 2005. He executed one of the largest value-generative technology separation transactions in history - the spinoff of Agilent from HP.

- Scott D. Cook founded the tax and accounting software company Intuit, where he served as President and CEO from 1984 until 1994. Under Scott's leadership, Intuit's revenues grew over 3,000% since its IPO.

- William C. Ford Jr. has been executive chairman of Ford Motor Company since September 2006 and was CEO of Ford from 2001 to 2006. Ford successfully navigated the financial crisis and emerged stronger than ever, having made tough but necessary restructuring choices before going into the downturn.

- Kathleen C. Mitic is founder and CEO of Sitch Inc. (formerly Three Koi Labs), a mobile startup. She previously held executive roles at leading technology firms such as Facebook, Palm, Zazzle and Yahoo.

- David M. Moffett was CEO of U.S. Bancorp from 1993 to 2007, where he was known for delivering prudent, long-term growth. He was asked to join Freddie Mac by the Federal Housing Finance Agency in late 2008 and helped them navigate the fiscal crisis until his retirement a year later.

- Pierre M. Omidyar founded eBay. He is still our largest shareholder, owning 8.5% of the company, and has established a framework on which eBay has delivered long-term shareholder value.

- Richard T. Schlosberg III was President and CEO of the David and Lucile Packard Foundation from 1999 until retirement in 2004. Prior to joining the foundation, he was Executive Vice President and Director of The Times Mirror Company, a media communications company, and Publisher and Chief Executive Officer of The Los Angeles Times. His investment expertise, derived from investing for the Foundation, has helped us identify and cultivate investments that can enhance or accelerate eBay's offerings in strategic areas and his knowledge and expertise in the communications industry is relevant to eBay's classified business.

- Thomas J. Tierney was the CEO of Bain & Company for over eight years, is co-founder of the Bridgespan Group, a non-profit advisor to philanthropic organizations, and a renowned author and expert on organizational leadership. He has helped us develop our talented eBay management team and has provided leadership to eBay and the board.

This exceptional board of entrepreneurs, executives and investors has a track record of taking decisive action, leading 37 acquisitions at eBay since 2008 as well as value-enhancing transactions as executives at their respective firms. The board has built a deep and strong management team that has driven eBay's consistent growth in revenue and profitability and that continues to deliver sustainable value to eBay shareholders.

The board has supported the management team in our turnaround and growth strategies. Over the past several years the board and management:

- Transformed eBay into a leading global commerce and payments company;

- Invested heavily in driving PayPal to a leadership position in digital and mobile payments. This includes expanding PayPal's global footprint, accelerating growth off of eBay, and making strategic acquisitions such as Bill Me Later and Braintree, which extend PayPal's product lines into important adjacent areas;

- Successfully transformed eBay Marketplaces from its traditional auction format to a more competitive, sustainable focus on fixed-price goods;

- Forged partnerships with leading retailers and brands;

- Enhanced the company's technology and innovation capabilities through acquisitions; and

- Made tough calls, reducing headcount, selling off underperforming assets and divesting Skype, a promising service that did not have the synergies with our core business that we had originally expected when we bought it.

At the same time, we’ve invested in new capabilities for the Marketplaces business. And we have moved aggressively to leverage PayPal’s integration with eBay to expand PayPal’s reach to millions of online retailers and to offline transactions. PayPal remains one of the fastest growing elements of the company – which helps explain why others are targeting the payments business but are far behind PayPal.

eBay and PayPal – Better Together

Our shareholders and our customers are best served by keeping PayPal and eBay together. No other payments competitor has achieved PayPal’s success – because no other competitor has had a commerce platform like eBay.

Why We Are Better Together:

- PayPal Grows Faster Because of eBay

- eBay Accelerates the Success of PayPal

- Data Sharing Leads to More Profitable Growth

- eBay Inc. Provides Efficient Capital for PayPal

- Commerce and Payments are Converging

Our commerce and payments businesses reinforce and support each other. Taking them apart would destroy value by reducing their considerable synergies, which cannot be easily replaced by arm’s length commercial agreements. Tightly integrated with eBay, PayPal can grow faster and more profitably than it would as a standalone company. Adoption and use of PayPal on eBay enables innovation and growth off of eBay. For example, eBay delivers about 30% of PayPal’s new users at virtually no cost, more than 30% of PayPal’s revenues and approximately 50% of PayPal’s profits. PayPal’s growth and leadership in mobile payments has occurred precisely because of this strong base of PayPal users on eBay.

As the commerce landscape evolves, we see even stronger synergies between PayPal and eBay. New users in the BRIC and emerging markets are an exciting part of this changing landscape. When PayPal expands into a new market like Russia or Brazil, established eBay customers provide PayPal a strong foundation to build a vibrant domestic business. Offline commerce is another new frontier for both eBay and PayPal, and moving offline together creates more powerful competitive advantages. Both businesses benefit from strong investment synergies in key areas of innovation, and the mobile-enabled commerce and payments markets remain vast and exciting opportunities.

We do not have a monopoly on good ideas. We know that. And we understand that we are operating in a dynamic environment. But Mr. Icahn is proposing nothing new. We have tested the idea of separation. Our board regularly reviews our businesses to determine the best course of action for the future. We have come to the conclusion that keeping PayPal as part of eBay is the right plan for today. However, as we have always done, we will continue reviewing the strategy and structure of our company with the best long-term interests of our shareholders clearly in mind.

Carl Icahn’s Shareholder Proposal and Proxy Fight

Mr. Icahn has nominated to your board two of his employees, Jonathan Christodoro and Daniel Ninivaggi, who have no relevant leadership or operational experience in technology. Both are overboarded under eBay's policies – both of them are already on four public company boards, and Mr. Ninivaggi is a Co-CEO of one of Mr. Icahn’s controlled companies. Mr. Christodoro is a recent graduate of business school with a few years of experience on Wall Street. He joined all four of his boards following Icahn pressure on those companies and has less than one year on average of experience on each board he has served on. Both individuals are contractually bound to Icahn affiliates and are required to hold business opportunities and investments in a fiduciary capacity for the benefit of those Icahn affiliates, preventing them from being truly independent directors. Mr. Icahn appears to have put little consideration into his selection of nominees to the eBay board, and we encourage shareholders to reject his unqualified nominees.

Rather than debate the merits of his proposal, Mr. Icahn has launched an aggressive media campaign to attack the management and directors of eBay. His distorted attacks, despite being the centerpiece of his campaign, have been disproven by the facts. Mr. Icahn has a long history of using personal attacks as a means to his own ends. We believe his public attacks have been counterproductive and are an attempt to distract attention from eBay’s long track record of delivering results for eBay’s shareholders.

More recently, Mr. Icahn has backed away from his proposal to spin off PayPal into a separately traded public company and from his arguments that PayPal would be more successful as a standalone company. He has announced a “new” idea – a carve-out IPO of PayPal. We’re glad to see that Mr. Icahn now seems to agree that a full separation of PayPal is not a good idea.

We are fully committed to always acting in the best long-term interests of our shareholders. We ask ourselves: Will a spinoff into a separately traded public company or even a partial spin make PayPal more competitive? Will it accelerate growth? Will it be possible without distracting PayPal’s innovation and execution at a critically important time? And, importantly, will it create sustainable value for shareholders over time? Today, we believe the answer to these questions is no – not now. PayPal and eBay are better together. In the future, our board will continue to evaluate all strategic options and make the right decisions for shareholders.

The bottom line is that Mr. Icahn is wrong about the quality of our board and he’s wrong about the best course today for PayPal. We oppose his unqualified board nominees, and we recommend that shareholders vote against his non-binding proposal to separate PayPal from eBay.

YOUR BOARD OF DIRECTORS REMAINS COMMITTED TO SERVING THE INTERESTS OF ALL EBAY SHAREHOLDERS – PLEASE VOTE THE WHITE PROXY CARD TODAY

Your board seeks your support electing the company’s four experienced nominees -- business leaders in technology with track records of delivering substantial shareholder value who have helped build the eBay success story -- on the WHITE proxy card: Fred Anderson, Edward Barnholt, Scott Cook, and John Donahoe. Please discard any proxy card sent to you by Mr. Icahn.

We are highly confident that eBay will remain a global leader in a connected commerce world. We believe PayPal will grow faster as part of eBay, and that eBay grows faster having PayPal. eBay’s strong positioning will benefit our customers, our employees, and you, our stockholders.

If you have any questions or need assistance voting eBay’s WHITE proxy card, please contact D.F. King & Co., Inc., which is assisting eBay, toll free at (800) 269-6427. Holders can find additional information regarding the 2014 annual meeting at https://bettertogether.ebayinc.com/.

On behalf of your Board of Directors, we thank you for your continued support.

Sincerely,

| Pierre Omidyar | Thomas Tierney | John Donahoe | ||||||||||||||||

| Chairman of the Board | Lead Independent Director | CEO | ||||||||||||||||

Non-GAAP Financial Measures

This communication includes the following financial measures defined as “non-GAAP financial measures” by the Securities and Exchange Commission (SEC): non-GAAP earnings per share and free cash flow. These measures may be different from non-GAAP financial measures used by other companies. The presentation of this financial information, which is not prepared under any comprehensive set of accounting rules or principles, is not intended to be considered in isolation of, or as a substitute for, the financial information prepared and presented in accordance with generally accepted accounting principles (GAAP). For a reconciliation of these non-GAAP financial measures to the nearest comparable GAAP measures, see the Appendix to this communication.

Forward-Looking Statements

This communication contains forward-looking statements relating to, among other things, the future performance of eBay and its consolidated subsidiaries that are based on the company's current expectations, forecasts and assumptions and involve risks and uncertainties. These statements include, but are not limited to, statements regarding expected financial results for the first quarter and full year 2014; the company's projected financial outlook for 2015; the future growth in the Payments, Marketplaces and Enterprise businesses and the company’s plans with respect to each of those businesses, mobile payments, mobile commerce; and the company's plans regarding its stock repurchase programs. The company's actual results could differ materially from those predicted or implied and reported results should not be considered as an indication of future performance. Factors that could cause or contribute to such differences include, but are not limited to: changes in political, business and economic conditions, including any continuing U.S. government shutdown or default, any European or general economic downturn or crisis and any conditions that affect ecommerce growth; fluctuations in foreign currency exchange rates; the company's need to successfully react to the increasing importance of mobile payments and mobile commerce and the increasing social aspect of commerce; the company's ability to deal with the increasingly competitive ecommerce environment, including competition for its sellers from other trading sites and other means of selling, and competition for its buyers from other merchants, online and offline; the company's need to manage an increasingly large enterprise with a broad range of businesses of varying degrees of maturity and in many different geographies; the effect of management changes and business initiatives; the company's need and ability to manage other regulatory, tax and litigation risks as its services are offered in more jurisdictions and applicable laws become more restrictive; any changes the company may make to its product offerings; the competitive, regulatory, credit card association-related and other risks specific to PayPal and Bill Me Later, especially as PayPal continues to expand geographically and introduce new products and as new laws and regulations related to financial services companies come into effect; the company's ability to timely upgrade and develop its technology systems, infrastructure and customer service capabilities, including our Enterprise Commerce Technologies, at reasonable cost; the company's ability to maintain site stability and performance on all of its sites while adding new products and features in a timely fashion; the company's ability to profitably integrate, manage and grow businesses that have been acquired or may be acquired in the future; the effect the announcement of the shareholder proposal and nominations may have on the company’s relationships with its shareholders and other constituencies and on the company’s ongoing business operations. The forward-looking statements in this communication do not include the potential impact of any acquisitions or divestitures that may be announced and/or completed after the date hereof.

More information about factors that could affect the company's operating results is included under the captions “Risk Factors” and “Management's Discussion and Analysis of Financial Condition and Results of Operations” in the company's most recent annual report on Form 10-K, a copy of which may be obtained by visiting the company's Investor Relations website at http://investor.ebayinc.com or the SEC's website at http://www.sec.gov. Undue reliance should not be placed on the forward-looking statements in this communication, which are based on information available to the company on the date hereof. The company assumes no obligation to update such statements.

| ($ In thousands, except percentages and per share amounts) | FY 03 | FY 04 | FY 05 | FY 06 | FY 07 | FY 08 | FY 09 | FY 10 | FY 11 | FY 12 | FY 13 | ||||||||||

| GAAP Operating Income | $629,241 | $1,059,242 | $1,441,707 | $1,422,956 | $613,180 | $2,075,682 | $1,456,765 | $2,053,571 | $2,373,491 | $2,888,483 | $3,371,423 | ||||||||||

| GAAP Operating Margin | 29.1% | 32.4% | 31.7% | 23.8% | 8.0% | 24.3% | 16.7% | 22.4% | 20.4% | 20.5% | 21.0% | ||||||||||

| Stock-based compensation expense | 5,492 | 5,832 | 31,772 | 317,410 | 301,813 | 352,042 | 394,808 | 381,490 | 457,186 | 487,646 | 608,742 | ||||||||||

| Employer payroll taxes on stock-based compensation / non-qualified stock options gains | 9,590 | 17,479 | 13,014 | 5,319 | 6,872 | 3,144 | 5,345 | 13,845 | 17,334 | 22,934 | 29,144 | ||||||||||

| Amortization of acquired intangible assets within cost of net revenues | - | - | - | 17,851 | 19,625 | 29,225 | 52,052 | 40,156 | 61,039 | 78,099 | 77,466 | ||||||||||

| Amortization of acquired intangible assets within operating expenses | 50,659 | 65,927 | 128,941 | 197,078 | 204,104 | 234,916 | 262,686 | 189,727 | 267,374 | 334,601 | 318,347 | ||||||||||

| Other | - | - | - | - | 1,390,938 | 49,119 | 381,386 | 21,719 | 57,582 | 29,387 | 2,303 | ||||||||||

| Non-GAAP Operating Income | 694,982 | 1,148,480 | 1,615,434 | 1,960,614 | 2,536,532 | 2,744,128 | 2,553,042 | 2,700,508 | 3,234,006 | 3,841,150 | 4,407,425 | ||||||||||

| Non-GAAP Operating Margin | 32.1% | 35.1% | 35.5% | 32.8% | 33.1% | 32.1% | 29.3% | 29.5% | 27.8% | 27.3% | 27.5% | ||||||||||

| GAAP Net Income | 441,771 | 778,223 | 1,082,043 | 1,125,639 | 348,251 | 1,779,474 | 2,389,096 | 1,800,962 | 3,229,388 | 2,609,440 | 2,856,078 | ||||||||||

| Stock-based compensation expense | 5,492 | 5,832 | 31,772 | 317,410 | 301,813 | 352,042 | 394,808 | 381,490 | 457,186 | 487,646 | 608,742 | ||||||||||

| Employer payroll taxes on stock-based compensation | 9,590 | 17,479 | 13,014 | 5,319 | 6,872 | 3,144 | 5,345 | 13,845 | 17,334 | 22,934 | 29,144 | ||||||||||

| Amortization of acquired intangible assets within cost of net revenues | - | - | - | 17,851 | 19,625 | 29,225 | 52,052 | 40,156 | 61,039 | 78,099 | 77,466 | ||||||||||

| Amortization of acquired intangible assets within operating expenses | 50,659 | 65,927 | 128,941 | 197,078 | 204,104 | 234,916 | 262,686 | 189,727 | 267,374 | 334,601 | 318,347 | ||||||||||

| Other | - | - | - | - | 1,390,938 | 49,119 | 381,386 | 21,719 | 57,582 | 29,387 | 2,303 | ||||||||||

| Interest and other income, net | (979) | (6,485) | (2,260) | - | - | - | - | 53,857 | (1,445,358) | (141,188) | (88,149) | ||||||||||

| Impairment of certain equity investments | 1,230 | - | - | - | - | - | - | - | - | - | - | ||||||||||

| Income taxes associated with certain non-GAAP entries | (18,595) | (31,520) | (50,517) | (171,690) | (165,421) | (202,975) | (12,067) | (202,760) | 23,006 | (321,260) | (248,374) | ||||||||||

| Cumulative effect of accounting change, net of tax | 5,413 | - | - | - | - | - | - | - | - | - | - | ||||||||||

| Non-GAAP Net Income | 494,581 | 829,456 | 1,202,993 | 1,491,607 | 2,106,182 | 2,244,945 | 3,473,306 | 2,298,996 | 2,667,551 | 3,099,659 | 3,555,557 | ||||||||||

| Diluted net income per share: | |||||||||||||||||||||

| GAAP | $0.67 | $1.14 | $0.78 | $0.79 | $0.25 | $1.36 | $1.83 | $1.36 | $2.46 | $1.99 | $2.18 | ||||||||||

| Non-GAAP | $0.75 | $1.21 | $0.86 | $1.05 | $1.53 | $1.71 | $2.66 | $1.73 | $2.03 | $2.36 | $2.71 | ||||||||||

| Shares used in GAAP diluted net income per share calculation | 656,657 | 683,860 | 1,393,875 | 1,425,472 | 1,376,174 | 1,312,608 | 1,304,981 | 1,327,417 | 1,312,950 | 1,312,556 | 1,312,733 | ||||||||||

| Shares used in Non-GAAP diluted net income per share calculation | 656,657 | 683,860 | 1,393,875 | 1,425,472 | 1,376,174 | 1,312,608 | 1,304,981 | 1,327,417 | 1,312,950 | 1,312,556 | 1,312,733 | ||||||||||

| ($ In millions) | FY 03 | FY 04 | FY 05 | FY 06 | FY 07 | FY 08 | FY 09 | FY 10 | FY 11 | FY 12 | FY 13 | ||||||||||

| Free Cash Flow | |||||||||||||||||||||

| GAAP operating cash flow | $874 | $1,285 | $2,010 | $2,248 | $2,641 | $2,882 | $2,908 | $2,746 | $3,274 | $3,838 | $4,995 | ||||||||||

| Purchases of property and equipment, net | (365) | (293) | (338) | (515) | (454) | (566) | (567) | (724) | (963) | (1,257) | (1,250) | ||||||||||

| Free cash flow | 509 | 992 | 1,672 | 1,732 | 2,187 | 2,316 | 2,341 | 2,022 | 2,311 | 2,581 | 3,745 |

About eBay Inc.

eBay Inc. (NASDAQ: EBAY) is a global commerce and payments leader, providing a robust platform where merchants of all sizes can compete and win. Founded in 1995 in San Jose, Calif., eBay Inc. connects millions of buyers and sellers and enabled $212 billion of commerce volume in 2013. We do so through eBay, one of the world's largest online marketplaces, which allows users to buy and sell in nearly every country on earth; through PayPal, which enables individuals and businesses to securely, easily and quickly send and receive digital payments; and through eBay Enterprise, which enables omnichannel commerce, multichannel retailing and digital marketing for global enterprises in the U.S. and internationally. We also reach millions through specialized marketplaces such as StubHub, the world's largest ticket marketplace, and eBay classifieds sites, which together have a presence in more than 1,000 cities around the world. For more information about the company and its global portfolio of online brands, visit www.ebayinc.com.

Contacts

eBay Inc.

Investor Relations Contact:

Tracey Ford

tford@ebay.com

Tom Hudson

thhudson@ebay.com

or

Media Relations Contact:

Abby Smith

press@ebay.com

or

Investor Information Request:

408-376-7493

or

Company News:

http://www.ebayinc.com/news

or

Investor Relations website:

http://investor.ebayinc.com

Source: eBay Inc.